Double Materiality - Part I

An overview and tips for the Environmental Standards.

What is Double Materiality? Why is it an essential part of the ESRS reporting process?

The CSRD establishes that the sustainability reporting under the legislation should be based on double materiality. This means that a company must conduct a double materiality assessment that considers both its (and its value chain(s)') impact on the environment and the external ( environmental and societal) impacts on its operations and value chain(s) to identify material impacts, risks, and opportunities (also referred to as IRO’s) and then utilize this assessment to decide what it should be reporting on in its sustainability report. The ESRS standards include 12 standards, two cross-cutting standards, five environmental, four Social, and one governance standard (as seen in the picture below).

The ESRS Standards

Irrespective of the outcome of their double materiality assessment, all companies have to apply the general requirements set in ESRS 1 and report on the following:

a) ESRS 2 General Disclosures

b) The Disclosure requirements and data points specified in the topical ESRS related to IRO-1 describe the process for identifying and assessing material impacts, risks, and opportunities.

c) AND If the company concludes that ESRS E1 Climate Change is not material and therefore omits all disclosure requirements under ESRS E1, it shall disclose a detailed explanation of how and why it came to this conclusion. This explanation should also include forward-looking information about what might lead the company to conclude that this will be material in the future. This detailed description of the materiality assessment process and the reasoning behind conclusions is optional when you omit other topics, but you may want to do so anyway. At the very least, you should have the materiality assessment documentation ready for the expected mandatory assurance process.

Everything else is subject to double materiality ….

————

For sustainability professionals and companies already used to materiality assessment processes and voluntary sustainability reporting, double materiality is a new and more holistic concept of sustainability materiality that integrates two perspectives. Double Materiality combines the impact materiality that companies might have become familiar with from reporting, according to GRI (Global Reporting Initiative), with the financial materiality that identifies information considered material for primary users of economic reports -something that companies might be familiar with from reporting on sustainability risks and opportunities by following the TCFD recommendations or by going through a CDP (Carbon Disclosure Project) or IFRS disclosure process. Therefore, companies with a previous impact assessment in alignment with GRI and/or companies that have gone through the process of preparing TCFD disclosures/IFRS/CDP can have an advantage when conducting double materiality assessments. Those with GRI experience might have a headstart regarding impact materiality. At the same time, those familiar with TCFD/IFRS/CDP disclosures might be better prepared for the Financial materiality assessment process. (If your enterprise is unfamiliar with voluntary sustainability reporting methods and all these acronyms, it might be a good idea to start by reading a GRI report, a CDP disclosure, and a TCFD report and understanding the different requirements and structures related to the various frameworks and standards.)

Impacts refer to the sustainability-related positive or negative impacts connected to the enterprise’s business operations and value chain. Actual and potential impacts should be identified through an impact materiality assessment.

Risks and opportunities refer to the company’s (the enterprise’s or “the undertaking’s” as the ESRS calls it) sustainability-related financial risks and opportunities, including those deriving from dependencies on natural, human, and social resources, as identified through a financial materiality assessment.

After identifying impacts, risks, and opportunities (IROs), companies have to assess their materiality. A sustainability subject is material when it meets the criteria for impact materiality, or financial materiality, or both.

Although there are no step-by-step requirements for conducting a double materiality assessment, the ESRS has certain criteria that should be considered in assessing materiality, and these are;

1) Actual negative impacts – for actual negative impacts, the materiality should be based on the severity of the impact, including:

a) the scale - how grave is the impact?

b) the scope - how widespread is the impact?

and

c) irremediable character – how easy is the negative impact to remediate?

2) Potential negative impacts – for potential negative impacts, the materiality should be based on the severity of the impact again, meaning:

a) the scale – how grave is the impact?

b) the scope – how widespread is the impact?

c) irremediable character- how easy is the negative impact to remediate?

and

d) the probability of the negative impact – how likely is the negative impact?

Negative impacts should be informed by the due diligence processes defined in the UN Guiding Principles for Businesses and Human Rights and the OECD Guidelines for Multinational Enterprises. In the case of HUMAN RIGHTS IMPACTS, the severity takes precedence over likelihood when identifying material topics (ESRS 1 paragraph 45)

3)Actual positive impacts – for actual positive impacts, the materiality should be based on severity only, including:

a) scale - how positive is the impact?

b) scope - how widespread is the positive impact?

4) Potential positive impacts- for potential positive impact, the materiality should be based on the severity and the probability (or likelihood), including:

a) scale - how positive is the impact?

b) scope - how widespread is the positive impact?

and

c) probability – how likely is the positive impact?

5)Risks and opportunities – the materiality of risks should be based on the combination of the probability of the occurrence and the magnitude of the financial effect.

Even though the CSRD does not prescribe a specific way to conduct a Double Materiality Assessment, it should be informed by the outcome of its due diligence process when this is in place (as defined by the UN Guiding Principles of Business & Human Rights and the OECD Guidelines for Multinational Enterprises on Responsible Business Conduct. The working group that helped develop the ESRS standards—EFRAG ( the European Financial Reporting Advisory Group)—has also published a guidance document that suggests how companies might conduct their double materiality assessment. This guidance recommends that companies follow a four-step process, as follows (Note that this guidance is not the final guidance and it has been under review/might be improved and updated):

1. Understanding the context (of your business and value chain) by:

a. Mapping out activities and business relationships. By analyzing the company’s business plan, strategy, financial statements, products, and services, as well as the geographic location of its business activities, companies can better understand and map out its upstream and downstream value chain. It can also help to look at the industry (or industries) where the company operates and analyze peers. This analysis can include existing sustainability reports, scientific articles, information on sector-specific benchmarks, or other publications on general sustainability trends.

b. Understanding affected stakeholders. Aim to uncover who will likely be affected by your company’s operations and upstream and downstream value chain. To understand and identify who your key stakeholders are:

i. Analyze existing stakeholder engagement initiatives (such as )

ii. Create a map of affected stakeholders across company activities and business relationships. Different parts of your value chain(s) and products/services might have unique and separate key stakeholders.

2. Identification of IROs related to sustainability matters by:

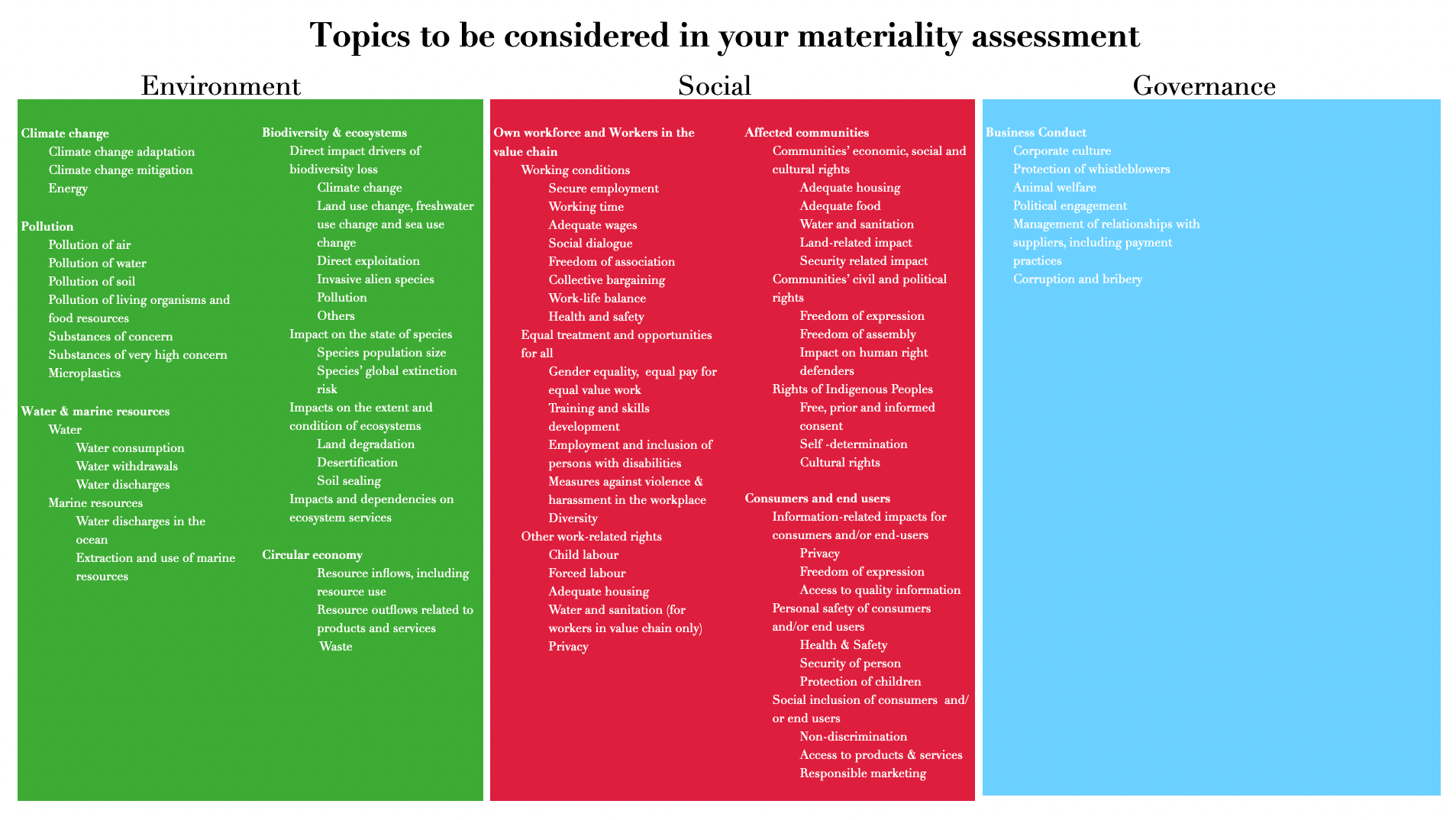

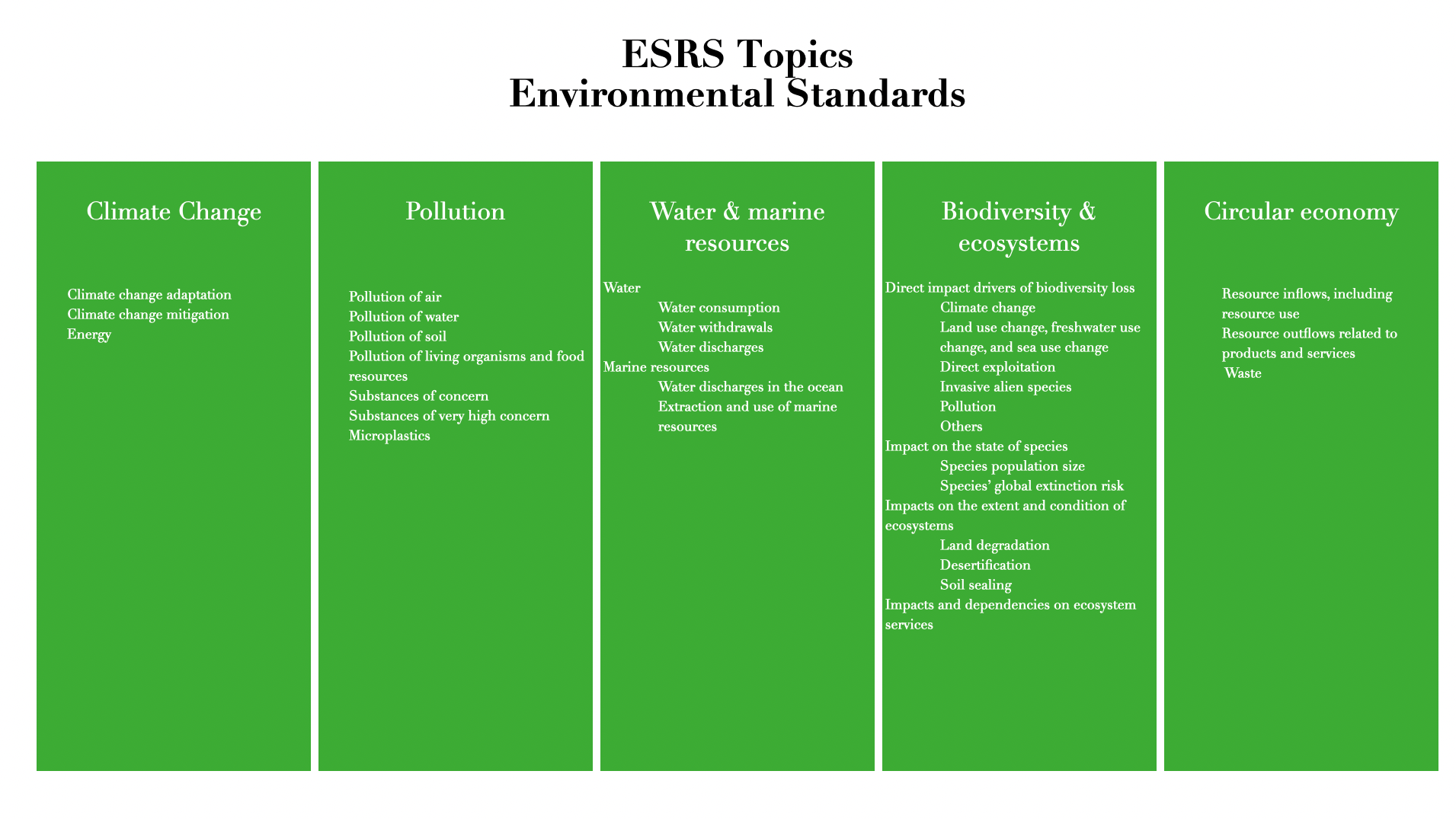

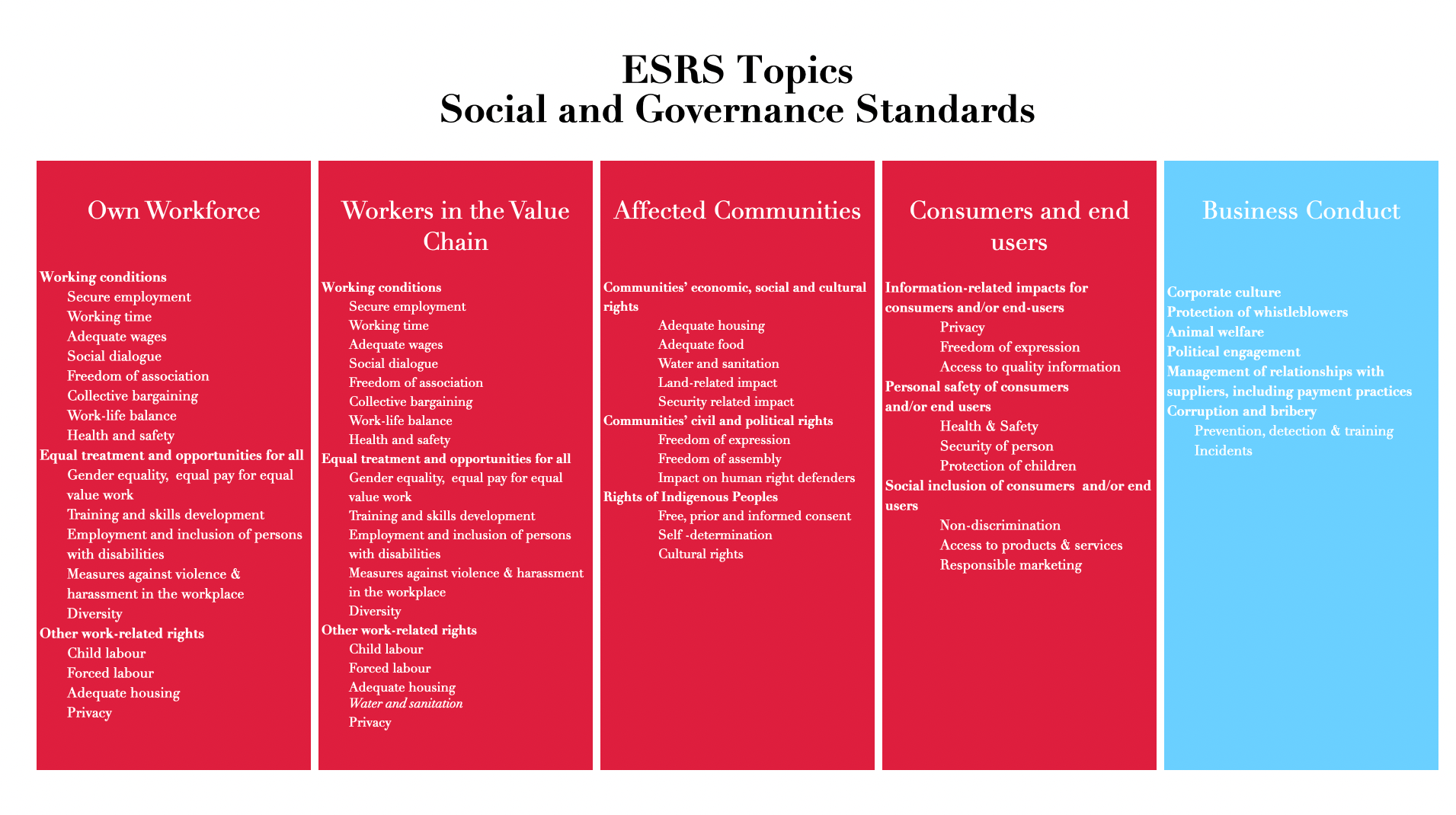

a. Considering the complete list from ESRS 1 paragraph AR 16 of sustainability topics to consider (see slideshow below);

b. AND do not forget to consider whether any topics are not covered sufficiently by the current ESRS sector agnostic standards. Suppose some topics are material for your company that are not adequately covered by the ESRS disclosures. In that case, you have to make your entity-specific disclosure on this topic. Until the ESRS sector standards are developed, it is recommended that companies look to current best practices on Industry-based guidance, such as the GRI Sector Standards and the SASB industry-based guidance, as examples and advice for this entity-specific requirement.

3. Assessment and determination of material IROs in these steps:

a. Conducting Impact materiality assessment

b. Conducting Financial materiality assessment

c. Consolidation of the outcome of the impact and financial materiality assessment.

4. Once the materiality assessment is complete, the company has to report on the process and its outcome due to the:

a. Disclosure requirement ESRS 2 IRO -1: Companies must describe their process for identifying and assessing material impacts, risks, and opportunities.

b. Disclosure requirement SBM-3: Requires companies to report how the identified material impacts, risks, and opportunities interact with the business model

c. Disclosure requirement IRO-2: This requirement requires companies to report on the Disclosure requirements in ESRS that the undertaking’s sustainability statement will cover. This disclosure also demands information on the thresholds and criteria utilized for assessing materiality.

Furthermore, Even though the ESRS does not mandate stakeholder engagement behavior, EFRAG recommends that engagement with the appropriate and affected stakeholders be a significant part of this process—consistent with international guidance on due diligence and responsible business conduct (e.g., the OECD Guideline for Multinational Enterprises on responsible business conduct and the UN Guiding Principles on Business and Human Rights). EFRAG recommends companies incorporate their stakeholders' views on the impacts, risks, and opportunities of their business activities, operations, and value chains. Engaging and consulting with affected stakeholders and subsequently incorporating their perspectives can help companies substantiate and decide on the relevance of sustainability matters. For example, Companies might want to consult with investors or banks on risks and opportunities and with workers in the value chain on human rights or adequate working conditions. (If consultation is not possible, or such interaction could put the stakeholder at risk, companies might want to consider interacting with subject matter experts such as NGOs representing the affected communities instead).

In addition to the guidance from EFRAG above and the emphasis on utilizing their due diligence process to guide the double materiality assessment process, I believe that the disclosure requirements related to the description of the process to identify and assess material topic-related impacts, risks, and opportunities (IRO-1) for each of the Environment related topical standard can be very helpful when assessing the materiality of the Environmental topics. The IRO-1 disclosures and their complementary Application requirements list elements companies have to describe whether and how they have considered in their materiality assessment process. This can, therefore, help guide the materiality assessment process for each of these topics. Below, I have used the IRO-1 disclosures related to each of the ESRS E1, E2, E3, E4, and E5 topical standards and their related Application Requirements to suggest how companies can use this as a guide for the kinds of elements to evaluate as part of their double materiality process.

ESRS E1 - Climate Change

To evaluate material impacts, risks, and opportunities related to Climate Change:

1. Evaluate GHG emissions – especially related to own operations.

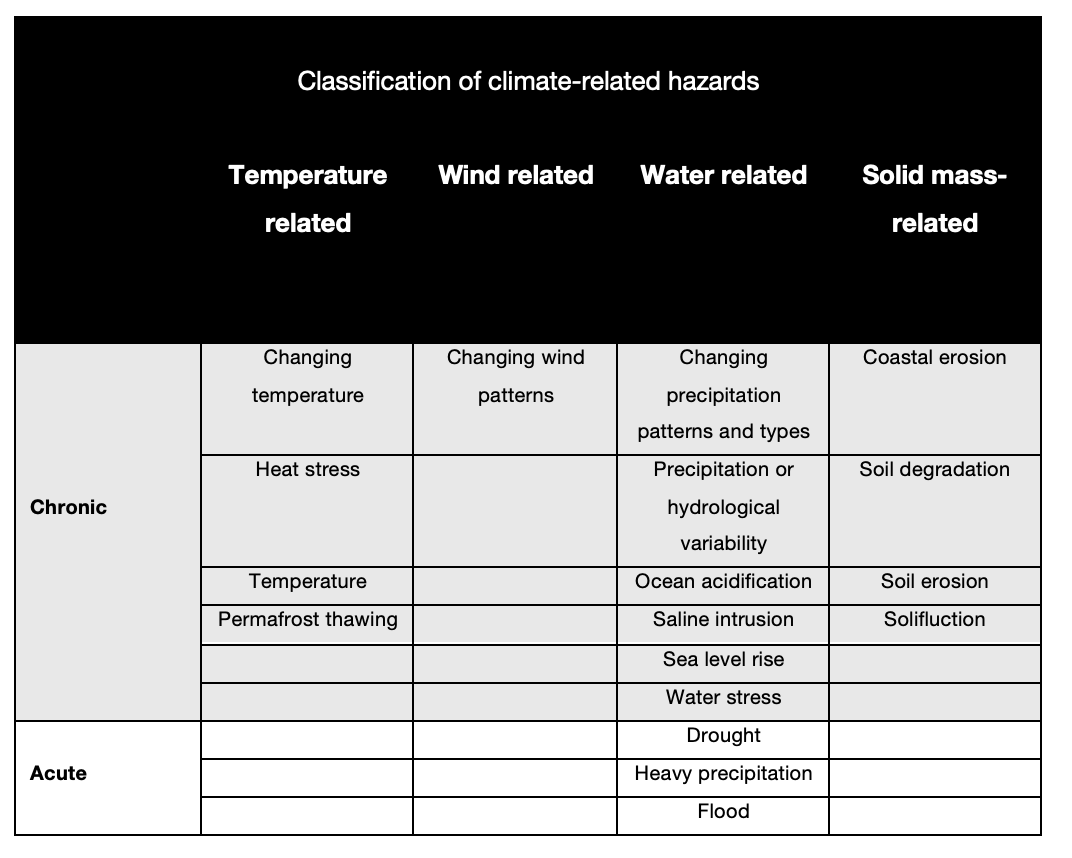

2. Evaluate climate-related physical risks and, more specifically, consider how your business activities might be exposed to or sensitive to the physical hazards in the table below (assuming at least a high-emission (or worst case) climate scenario) :

Table 1 : Climate hazards

3. Evaluate climate-related transition risks and opportunities and, more specifically, consider how your business activities may be exposed to these transition events (see examples in the table below), assuming at least a climate scenario in line with limiting global warming to 1.5C :

Table 2: Climate related transition risks (examples)

4. Evaluate whether and how assets or business activities are not in line with a transition to a climate-neutral economy.

Pollution

To evaluate material impacts, risks, and opportunities related to Pollution:

Evaluate site locations where pollution could be material and/or business activities associated with pollution in the company’s operations and the upstream and downstream value chain(s) to identify material actual and potential pollution-related impacts, risks, and opportunities. One suggested way to do this is to conduct a LEAP (Locate, Evaluate, Assess, and Prepare) assessment:

Locate: Locate where, in the company’s own operations and value chain, pollution of air, water, and soil occurs, as well as the sectors and business units related to those emissions or the production, distribution, use, or import/export of microplastics, substances of concern, and substances of very high concern, (on their own or in mixtures or articles).

Evaluate: Evaluate the company’s impacts and dependencies for each site or sector/business unit, including the severity and likelihood of the impacts on the environment and human health.

Assess*: Assess the material risks and opportunities based on a) and b) by identifying:

1. Transition risks and opportunities in own operations and value chain related to:

a. Policy and legal: For example, new regulation or legislation on pollution, sanctions/litigation related to pollution, or enhanced reporting on chemicals and emissions.

b. Technology: For example, the substitution of current products and services by-products with a lower impact, or the transition away from substances of concern,

c. Market: For example, a shift in demand and financing or increased costs of some substances.

d. Reputation: For example, changing customer perception and behavior due to the organization’s role in pollution prevention and control.

2. Physical risks in your own operations or value chain, for example, sudden interruptions of access to clean water, acid rain, or other pollution events that are likely to lead to significant pollution with subsequent significant effects on the environment and society;

3. Opportunities related to pollution control and prevention caused by:

a) Recourse efficiency: For example, decreased quantities of substances used or improved production processes and efficiency to minimize impact.

b) Markets: For example, a new non-toxic product line that focuses on eliminating substances of concern.

c) Financing: For example, access to green funds, bonds, or loans.

d) Resilience: For example, diversification of substances used and control of emissions through innovation or technology; and;

e) Reputation: For example, positive stakeholder responses to the company’s proactive stance on managing pollution-related risks.

*AND If relevant, always consult with affected communities or stakeholders when completing the assessment.

4. Prepare: Prepare and report the results of the materiality assessment. When providing information on the outcome of the materiality assessment, the undertaking has to consider:

a) A list of site locations where pollution is a material issue for the company’s operations and its upstream and downstream value chain and

b) A list of business activities associated with material impacts, risks, and opportunities related to pollution.

Water and Marine Resources

To evaluate material impacts, risks, and opportunities related to Water & marine resources:

Evaluate site locations where water and marine resources could be a material and/or relevant business activities associated with water & marine resources in the company’s operations and the upstream and downstream value chain(s) to identify material actual and potential water & marine resource-related impacts, risks, and opportunities. One suggested way to do this is to conduct a

LEAP (Locate, Evaluate, Assess, and Prepare) assessment:

Locate: Identify supplier sites, own operational sites, and value chain sites within areas of water stress (and especially areas of high water stress) and find the areas where the business interfaces with marine resources, as well as the sectors or business units that interact with water or marine resources in these areas.

Evaluate: Then evaluate the dependencies and impacts of each priority location/business activity by identifying business processes and activities that lead to consequences for and dependencies on environmental assets and ecosystem services.

For water-related impacts, evaluate the consumption of surface water, groundwater, water discharges, water withdrawals, and the effects on river basins. To consider the status of water bodies, you can use the relevant annexes of Directive 2000/60/EC (Water Framework Directive) and guidance from the Water Framework Directive.

For marine resource-related impacts, consider the extraction of marine resources and any potential dependencies on key marine resources or related commodities like seafood and gravel. Examples of marine resource dependencies include commercially exploited fish, shellfish, or fishing activity involving mobile bottom trawling, which can negatively impact the seabed. To consider marine resource dependencies, you may use international classifications such as the Common International Classification of Ecosystem Services (CICES).

After reviewing your operations, identify water and marine resources-related impacts and dependencies across your value chain by considering the same elements you considered within your business and operations (above).

Assess the severity and likelihood of the positive and negative impacts on water and marine resources that you have identified.

Assess* the material risks and opportunities by identifying and assessing:

1) Transition risk and opportunities in own operations and value chain related to:

a. Policy and legal: For example, risks related to new policies for increased water protection, ineffective water governance policies, marine resource policies resulting in water or ocean degradation, risks of exposure to sanctions or litigation, or enhanced reporting regulations.

b. Technology: For example, the substitution of products or services due to the transition to more efficient and cleaner technologies with a lower impact on water and marine resources, the introduction of new monitoring technologies, or the introduction of other technologies like flood mitigation or water purification technology.

c. Market: For example, shifting supply, shifts in demand and financing, or volatility and increased costs of water and marine resources.

d. Reputation: For example, changing societal, customer, or community perceptions as a result of your organization’s impact on water and marine resources and

e. Contribution to systemic risk: For example, the risk that a marine ecosystem collapses or that a natural system no longer functions because tipping points are reached or physical risks occur.

2) Physical risks including water quantity (water stress and scarcity), water quality, infrastructure decay, and the unavailability of some marine resource-related commodities.

3) Opportunities related to

a. Resource efficiency: For example, the transition to more efficient services and processes that require less water and marine resources.

b. Markets: For example, the development of less resource-intensive products and services and, thus, diversification of business activities.

c. Financing: For example, access to green funds, bonds, or loans.

d. Resilience: For example, diversification of marine or water resources and business activities by starting a new business unit on ecosystem restoration, investing in green infrastructure or nature-based solutions, or adopting circularity mechanisms that reduce the dependencies on water and marine resources.

e. Reputation: For example, positive stakeholder engagement as a result of the proactive stance on managing water and marine resource-related risks.

*AND If relevant, always consult with affected communities/stakeholders when completing the LEAP assessment.

4) Prepare: Prepare and report the results of the materiality assessment. When providing the information on the outcome of the materiality assessment, the company has to consider the following:

a) A list of geographical areas where water is a material issue for the enterprises’ operations and its upstream and downstream value chain;

b) A list of marine resources-related commodities used by the company that are material to the good environmental status of marine waters as well as for the protection of marine resources; and;

c) A list of sectors or segments associated with water and marine resources material impacts, risks, and opportunities.

Biodiversity and Ecosystems

To evaluate material impacts, risks, and opportunities related to Biodiversity and ecosystems:

Evaluate site locations where biodiversity and ecosystem impact could be material and/or relevant business activities associated with biodiversity and ecosystems in the company’s operations and the upstream and downstream value chain(s) to identify material actual and potential biodiversity and ecosystem-related impacts, risks, and opportunities. One suggested way to do this is to conduct aLEAP (Locate, Evaluate, Assess, and Prepare) assessment:

Locate: Identify locations within your operations and value chain relevant to your business activities. List the biomes and ecosystems these locations are interfacing with and find out the current integrity & importance of biodiversity and ecosystems at each location. Create a list of places where your company is near biodiversity-sensitive areas and find out whether activities related to these areas are negatively affecting the biodiversity-sensitive area or causing disturbance of the habitats or species for which a protected area has been designated. For example, by using tables like this:

Tables 3 and 4: Table representation of Biodiversity and ecosystem information.

Identify which sectors, business units, value chains, or asset classes are interfacing with biodiversity and ecosystems in these material sites. Alternatively, you can identify how sectors, business units, value chains, or asset classes are interfacing with biodiversity and ecosystems per raw material procured or sold in tons. For example, by using a table like this:

Table 5: Raw materials and their sourcing -impacts on biodiversity and ecosystems.

Evaluate: Then evaluate actual and potential impacts and dependencies of each priority location/business activity/raw material by Identifying business processes and activities that lead to consequences for and dependencies on biodiversity and ecosystem services and indicating the size, scale, and frequency of occurrence, as well as, the timeframe of the impacts by for example disclosing/understanding;

a) The percentage of suppliers that are located in risk-prone areas with threatened species (species on the IUCN red list of species, the Birds and Habitats Directive, national list of threatened species, or species in officially recognized protected areas like the Natura 2000 Network of Protected Areas, or in Key Biodiversity Areas.)

b) The percentage of its procurement spend from suppliers with facilities in risk-prone areas (with threatened species on the IUCN red list of species, species on the birds and habitat directive, national list of threatened species, or species in an officially recognized protected area like the Natura 2000 Network of Protected Areas or in a Key Biodiversity Area.

c) Indicate the size and scale of the dependencies on biodiversity and ecosystems, including raw materials, natural resources, and ecosystem services. Companies can examine dependencies on ecosystem services using the International Classifications of Ecosystem Services.

ESRS suggests using tables to present the information like this:

Table 6 and 7: Dependencies and Impacts related to Biodiversity and ecosystems.

Assess* material risks and opportunities by identifying and assessing:

1) Transition risk in own operations and value chain, including:

a. Policy and legal: For example, risks related to new policies for increased land protection, exposure to litigation due to spills of polluting effluents that damage human and ecosystem health, violations of biodiversity-related rights, violations of permits/ allocations, or negligence towards /killing of threatened species.

b. Technology: For example, the substitution of products or services with new, lower-impact products, the lack of technology or access to data to sufficiently capture high-quality biodiversity-related assessments, or the introduction of new monitoring technology.

c. Market: For example, shifting supply, shifts in demand and financing, or volatility and increased costs of raw materials due to changes in biodiversity/ecosystem health.

d. Reputation: For example, changing societal, customer, or community perceptions due to your organization’s impact on biodiversity, violations of nature-related rights, or effects on endangered species.

2) Physical risks including:

a. Acute risks, for example, natural disasters exacerbated by the loss of coastal protection from ecosystems, leading to costs of storm damage to coastal infrastructure, a disease affecting the species or variety of crops the company relies on, low genetic diversity, and ecosystem degradation; and

b. Chronic risks, for example, the loss of crop yield due to a decline in pollination services, increasing scarcity or variable production of key natural inputs, and ecosystem degradation due to operations (like desertification, soil degradation, deforestation, ocean acidification, or coastal erosion).

3) Systemic risks, including:

a. Ecosystem collapse—risks related to the potential of a natural system no longer functioning. This can occur when tipping points have been reached, and the collapse of ecosystems results in sector losses or geographical losses.

b. Aggregated risk linked to fundamental impacts of biodiversity loss across one or more sectors in a portfolio ( corporate or financial)

c. Contagion risks - systematic risks caused by certain corporations or financial institutions’ failure to account for biodiversity-related risks.

4) Opportunities related to;

a. Resource efficiency: For example, the transition to more efficient services and processes that require less impact on biodiversity.

b. Markets: For example, the development of less resource-intensive products and services and the diversification of business activities.

c. Financing: For example, access to green funds, bonds, or loans.

d. Sustainability performance: For example, opportunities related to restoration, regeneration, and the sustainable use of natural resources.

e. Reputation: For example, positive stakeholder engagement resulting from a proactive stance on managing biodiversity and ecosystem-related impacts, risks, and opportunities.

*AND If relevant, always consult with affected communities when completing the LEAP assessment.

5) Prepare: Prepare and report the results of the materiality assessment. When providing the information on the outcome of the materiality assessment, the company has to consider the following:

a) Whether or not it has sites located near biodiversity-sensitive areas and whether the activities related to these sites affect these areas by deteriorating the natural habitats or disturbing the species for which a protected area has been designated.

b) Whether it has identified any need to implement biodiversity mitigation measures such as those mentioned in:

a) Directive 2009/147/EC on the conservation of birds

b) Directive 92/43/EEC on the conservation of natural habitats and wild flora and fauna,

c) Directive 2011/92/EU on European Parliament of the Council, or;

d) Other international standards such as the International Finance Corporation (IFC) Performance Standard 6: Biodiversity Conservation and Sustainable Management of Living Natural Resources.

Resource Use & Circular Economy

To evaluate material impacts, risks, and opportunities related to Resource use and circular economy:

Evaluate activities and locations in the company’s operations and the upstream and downstream value chain(s) to identify material actual and potential resource and circular economy-related impacts, risks, and opportunities. One suggested way to do this is to conduct a LEAP (Locate, Evaluate, Assess, and Prepare) assessment:

Locate and evaluate: Rely on the analysis conducted under the materiality assessments of ESRS E1 Climate, ESRS E2 Pollution, and ESRS E3 Water & marine resources as well as ESRS E4 Biodiversity and ecosystems to identify and evaluate how your company’s operations and value chain(s) contributes to resource use and whether or not this utilization of resources is aligned with a circular economy. A circular economy aims to reduce the environmental impact of using products, materials, and other resources, minimizing waste and the use/release of harmful substances – and, therefore, the effect on nature. Assess the severity and likelihood of your resource use's positive and negative impacts.

Assess* material risks and opportunities by identifying and assessing:

1) Transition risk in own operations and value chain, including the risk of staying in a business-as-usual scenario while considering:

a. Policy and legal transition risks: For example, bans on extracting non-renewable resources and regulations on waste treatment.

b. Technology transition risks: For example, the introduction of less resource-intensive products and services in your niche.

c. Market transition risks: For example, shifts in the supply of raw materials, demand for less resource-intensive alternatives, and financing.

d. Reputational risks: For example, changes in customer preferences and customer or community perceptions related to your company's resource intensity.

2) Physical risks including the depletion of stock and use of virgin and non-virgin renewable resources.

3) Opportunities related to

a. Resource efficiency: For example, the transition to more efficient services and processes that require fewer resources: ecodesign for longevity, repair, reuse, takeback systems, remanufacturing, and refurbishing.

b. Markets: For example, demand for less resource-intense products and services, and new consumption models such as products as a service, pay-per-use, sharing, or leasing.

c. Financing: For example, access to green funds, bonds, or loans.

d. Resilience: For example, diversification of resources and business activities (new business units focused on recycling or refurbishing), investing in circularity mechanisms that help reduce resource dependencies, and managing changes in stocks and flows of resources.

e. Reputation: For example, positive customer feedback or enhanced reputation after initiating new circular business models.

*AND If relevant, always consult with affected communities when completing the assessment.

4) Prepare: Prepare and report the results of the materiality assessment. When providing the information on the outcome of the materiality assessment, the company has to consider the following:

a) A list of business units associated with resource use and circular economy material impacts, risks, and opportunities in the context of the undertaking's products and services and the waste it generates.

(b) A list and prioritization of the material resources the undertaking uses.

(c) The material impacts and risks of staying in business as usual.

(d) The material opportunities related to a circular economy.

(e) The material impacts and risks of a transition to a circular economy.

(f) The value chain stages where resource use, risks, and negative impacts are concentrated.

Once a sustainability matter has been evaluated as material, the company will have to report on the information prescribed by all the disclosure requirements related to policies, actions, and targets in the relevant topical ESRS (or, when they become available, the appropriate sector ESRS, or for entity-specific disclosures the minimum disclosure requirements for policies, actions, and targets ) that are related to that material sustainability matter. If the company has yet to adopt any policies, actions, or targets for this sustainability matter, it can simply state that this is the case (and does not have to but can provide a timeline for when it aims to have these in place). For metrics related to material sustainability topics, the company must include the information prescribed by the disclosure requirement only if it assesses the information to be material. If the company does not think the metric is needed to meet the objective of the disclosure requirement, it can omit the metric.

Unlike the environmental standards, the social and governance standards do not have detailed, specific disclosure elements under IRO-1. My next post will, therefore, focus more on due diligence in more detail and explain some tips on elements to consider when considering double materiality for these standards...

If you read this far, I would love to hear your opinion on this post! Did you think it was useful? What do you think about the ESRS requirements for double materiality? Do you think implementing the Double Materiality perspective will significantly change how companies think about sustainability in their operations and value chains?