Sustainability Due Diligence & Double Materiality Part II

Double Materiality Part II - Due Diligence, Social and Governance Standards

Following my previous post, which explored Double Materiality and the climate standards, this post delves deeper into how the double materiality assessment process is tied to sustainability due diligence and offers some tips for the double materiality assessment in relation to ESRS’s social and governance topics.

In the previous post, we established that the basis for evaluating whether to report on sustainability topics should be the Double Materiality Assessment (If you have not read the previous post, I recommend reading this post that gives an overview of Double Materiality under ESRS and more specific tips for the climate standards first). The Double Materiality process is the process of uncovering and assessing the positive and negative impacts as well as financial risks and opportunities associated with each sustainability topic. But how do you do that in practice, and how can you do it effectively, especially for the social and governance topics under ESRS?

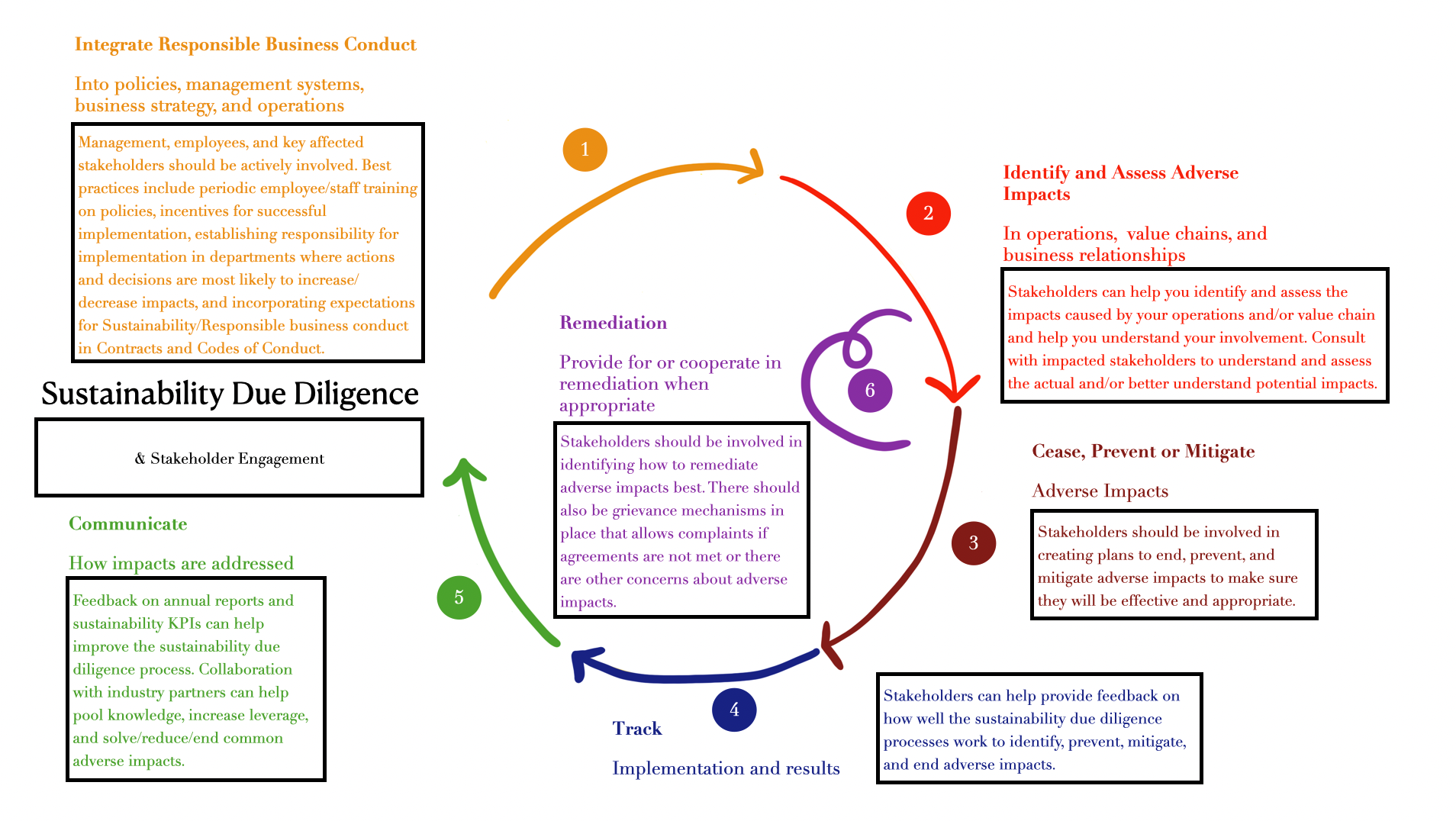

The basis of the Double Materiality Assessment process should be Sustainability Due Diligence. The OECD Due Diligence Guidance for Responsible Business Conduct gives a good overview of what this is, and in the slideshow below, I have summarized key takeaways from this guidance. Below is a slideshow that I hope can help give you a nice overview of sustainability due diligence and how it is connected to the ESRS, as well as the ESRS definitions of stakeholders and some best practices for stakeholder engagement in the due diligence process:

Slide 1:

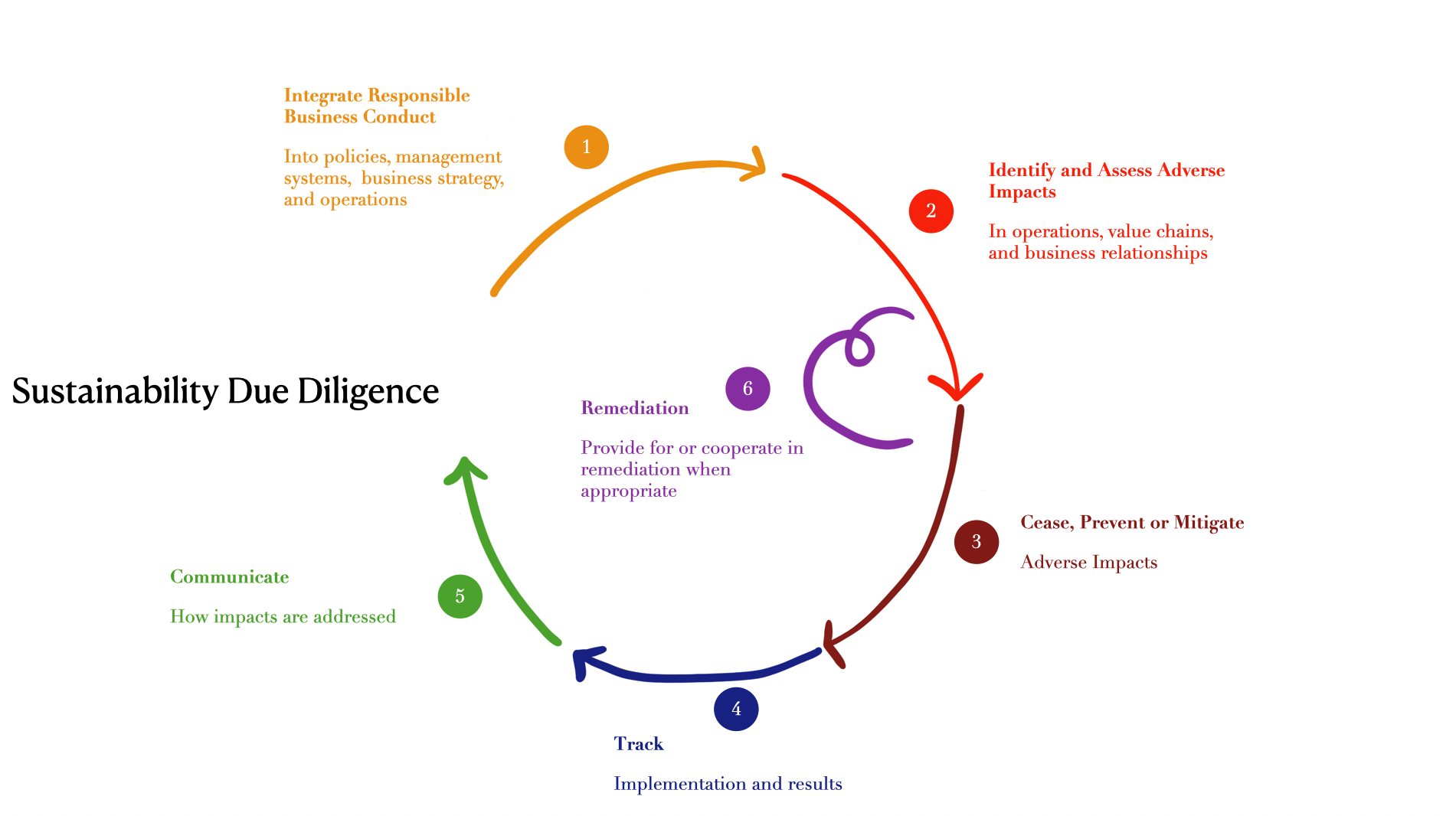

Sustainability Due Diligence can be described as a 6-step process that involves [1]:

1) Integrating/Embedding Responsible Business Conduct/Sustainability Due Diligence into policies, management, business strategy and operations.

2) Identifying and assessing adverse impacts (under ESRS, this would be called material impacts) in operations, value chains (not only supply chains, but the entire value chains), and business relationships

3) Ending, Preventing or Mitigating adverse impacts

4) Tracking implementation and results

5) Communicating how impacts are addressed

6) Providing remediation or cooperating in remediation when appropriate

Slide 2:

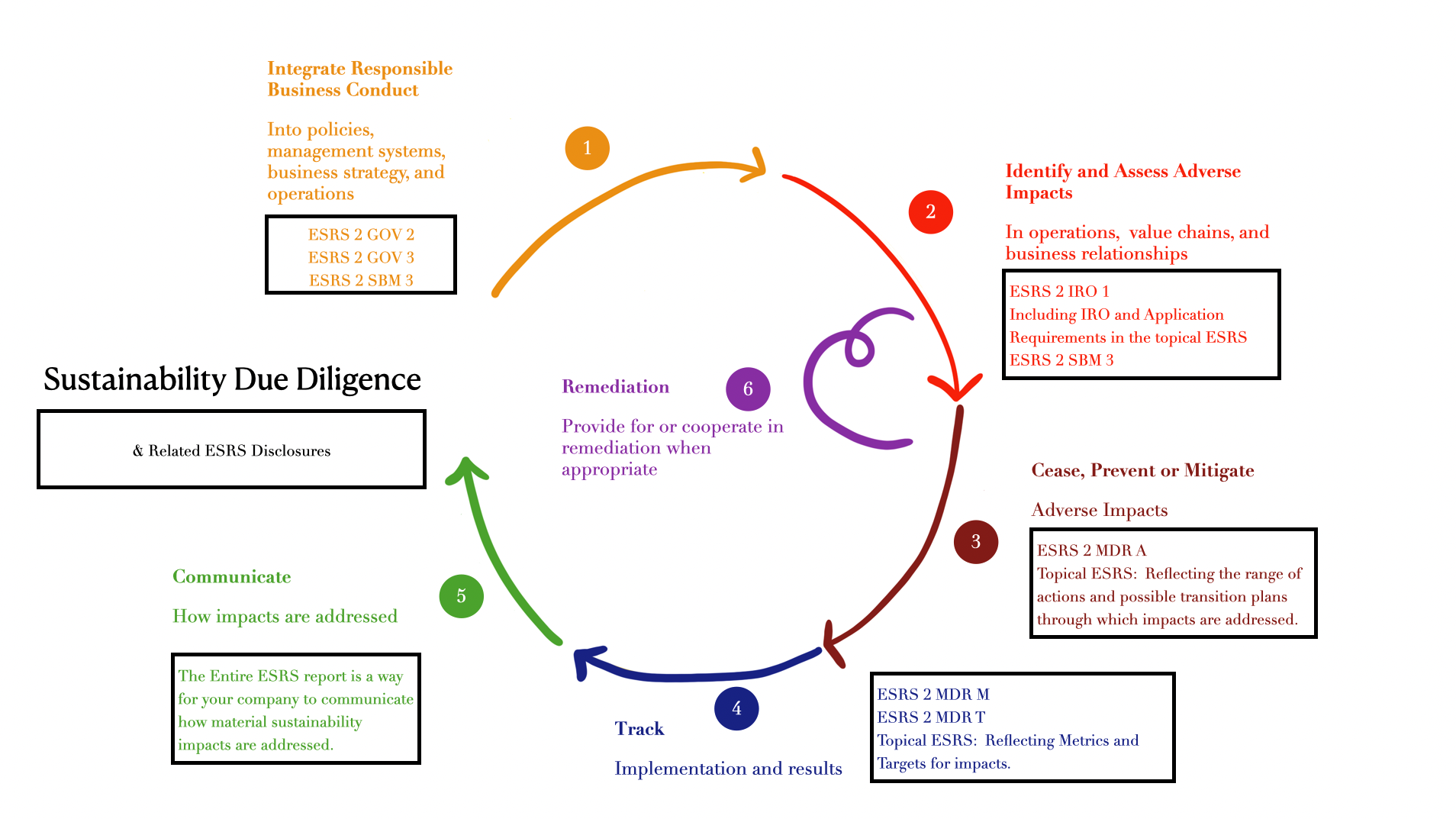

The disclosure requirements under ESRS correspond to the different steps in sustainability due diligence. They are designed to help readers of your sustainability report/sustainability statement assess how well you have implemented these steps and to help them follow your progress and actions towards the sustainability goals that you have set out.

Slide 3:

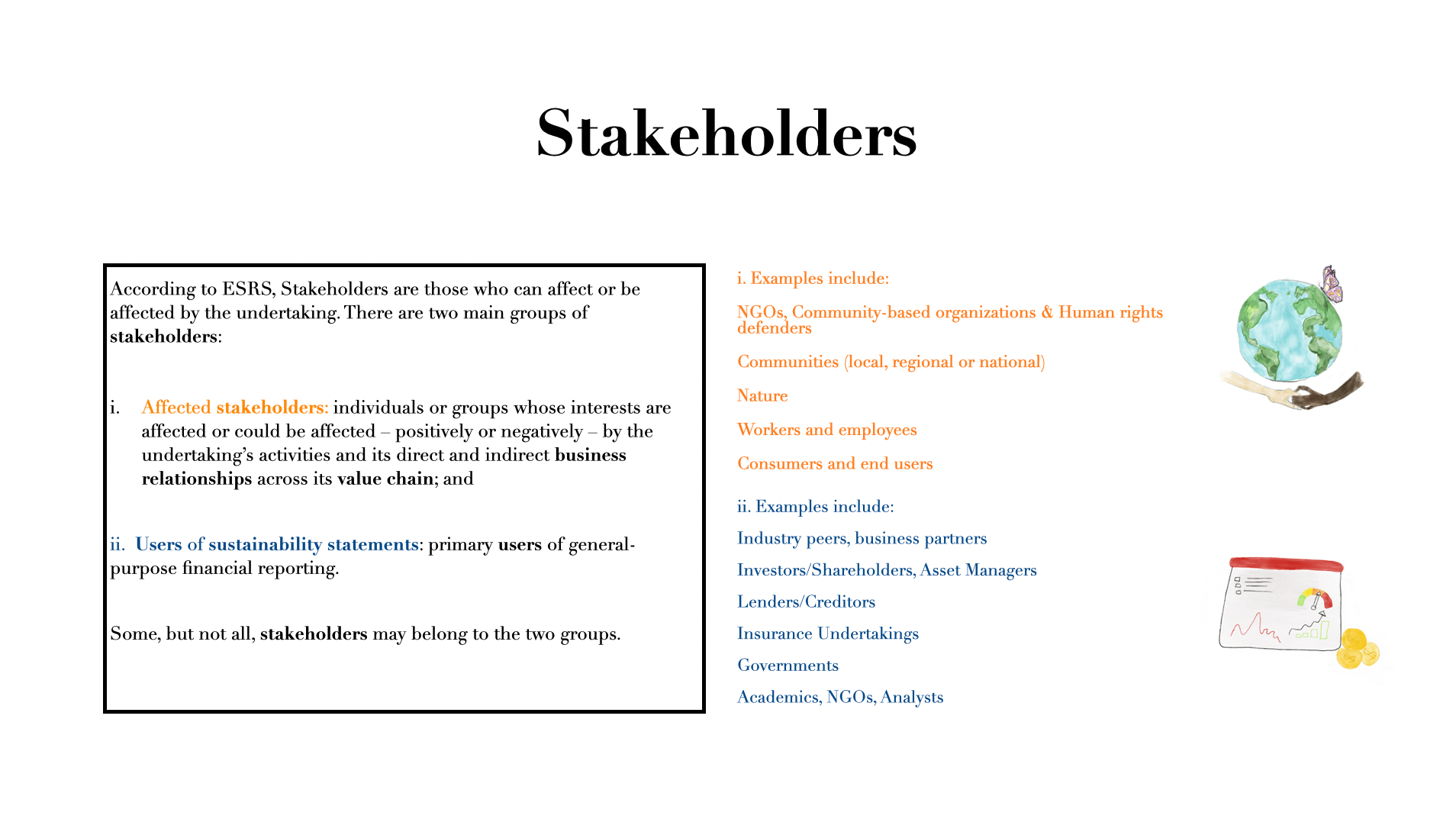

Stakeholders should be involved throughout this process. ESRS has a specific definition of stakeholders, including affected stakeholders and users of sustainability statements. In essence, stakeholders are the people (and/or the nature) affected by your business operations and/or your value chain.

Slide 4:

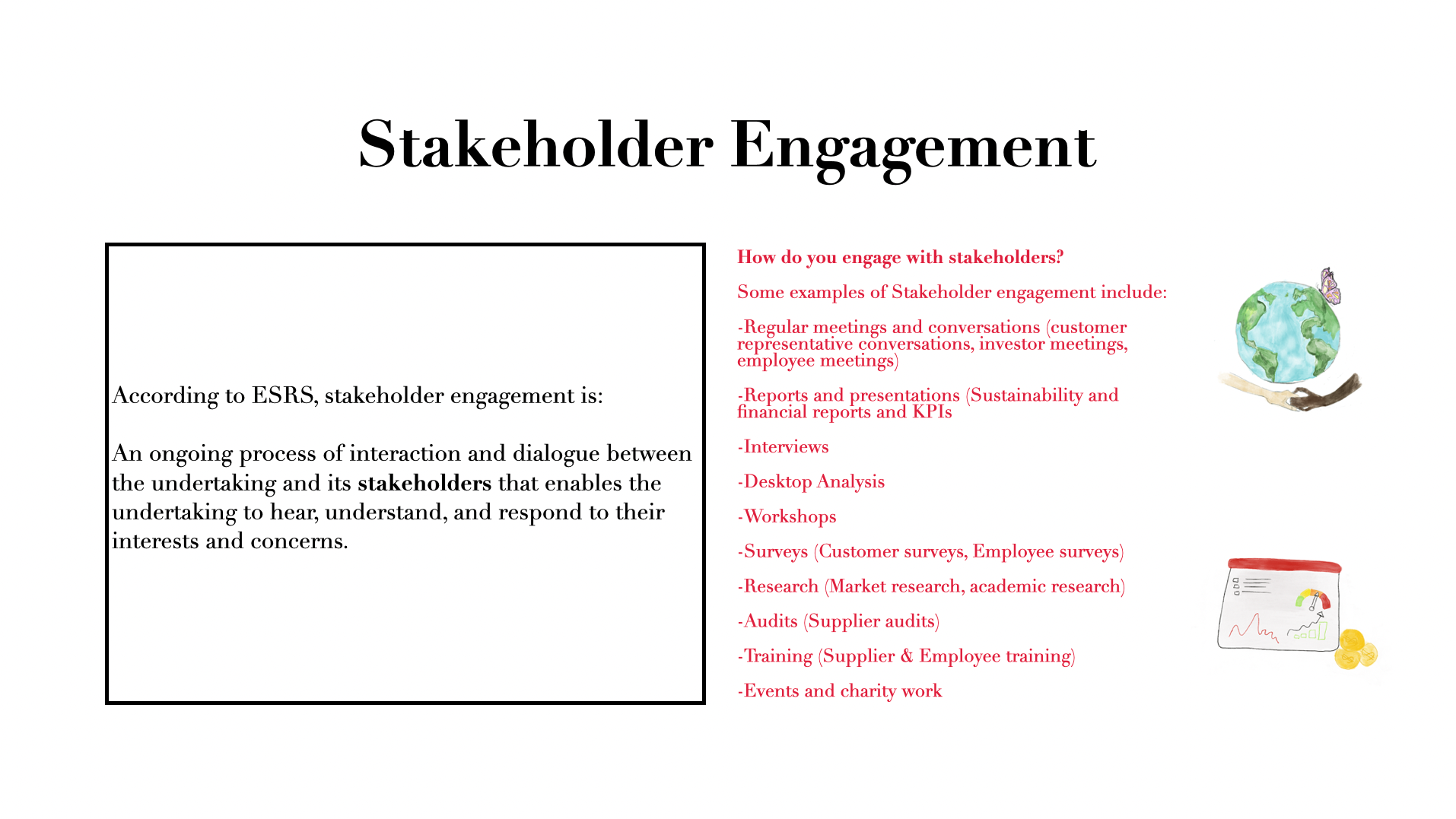

Stakeholder engagement is an ongoing process that involves the people impacted by your operations and value chain in the conversation (and potentially decision-making) so that you can better understand and reduce your negative impacts and risks and, hopefully, also create more positive impacts and generate opportunities!

Slide 5:

Stakeholders can be involved throughout the Due Diligence process in many ways.

Now for some specific thoughts on the Double Materiality Process for the Social & Governance Topics of ESRS :

When evaluating the double materiality of the social topics in ESRS, you must at least consider your Own Workforce, Workers in the Value Chain, Affected Communities, Consumers, and End Users. For governance, companies have to consider Business Conduct. The visual below shows the related sub-topics & sub-subtopics for each of these categories:

As you will see in the detailed overview below, a common theme among all these standards and topics is the emphasis on alignment with and the protection of human rights. In my previous post (the description of the criteria for double materiality, which is repeated here in the Red text), the materiality of negative human rights impacts should always be evaluated with an emphasis on the severity (before the likelihood of the impact). I have, therefore, also made this list of international conventions on human rights/ILO conventions and EU directives that are connected to the topics of each standard to help you better evaluate any potential material impact related to these :)

And as we recall from my last post:

Although there are no step-by-step requirements for conducting a double materiality assessment, the ESRS has certain criteria that should be considered in assessing materiality, and these are;

1)Actual positive impacts – for actual positive impacts, the materiality should be based on severity only, including:

a) scale - how positive is the impact?

b) scope - how widespread is the positive impact?

2) Potential positive impacts- for potential positive impact, the materiality should be based on the severity and the probability (or likelihood), including:

a) scale - how positive is the impact?

b) scope - how widespread is the positive impact?

and

c) probability – how likely is the positive impact?

3)Risks and opportunities – the materiality of risks should be based on the combination of the probability of the occurrence and the magnitude of the financial effect.

4) Actual negative impacts – for actual negative impacts, the materiality should be based on the severity of the impact, including:

a) the scale - how grave is the impact?

b) the scope - how widespread is the impact?

and

c) irremediable character – how easy is the negative impact to remediate?

5) Potential negative impacts – for potential negative impacts, the materiality should be based on the severity of the impact again, meaning:

a) the scale – how grave is the impact?

b) the scope – how widespread is the impact?

c) irremediable character- how easy is the negative impact to remediate?

and

d) the probability of the negative impact – how likely is the negative impact?

Negative impacts should be informed by the due diligence processes defined in the UN Guiding Principles for Businesses and Human Rights and the OECD Guidelines for Multinational Enterprises. In the case of HUMAN RIGHTS IMPACTS, the severity takes precedence over likelihood when identifying material topics (ESRS 1 paragraph 45)

Overview of Own Workforce:

The objective of the Own Workforce standard is to enable users of the sustainability report to understand how the company depends on and impacts its employees in their operations, including how well the company complies with international human rights instruments, as well as the financial impact of this. Disclosure requirements in the standard will ask for your company’s policies related to your workforce, the approach to human rights, engagement with your workforce, measures to remedy human rights impacts, and how these processes and policies are monitored. The Disclosure requirements will also ask whether these policies and processes are aligned with guidelines such as the OECD Guidelines for Multinational Enterprises. Under the Disclosure requirement SBM-3, the standard also specifically asks for operations at significant risk for incidents of forced labor, compulsory labor, and child labor. Appendix A.1 of the standard also gives you some examples of factors you should consider in the double materiality assessment related to your own workforce.

So, what are some examples of things to consider during the double materiality assessment process, as well as some examples of impacts, risks, and opportunities related to the sub-topics and sub-sub-topics under Own Workforce?

Let's go over the different sub-topics and sub-subtopics under Own Workforce one by one.

Working conditions:

Examples of possible positive Impacts related to Working conditions (Own workforce):

1. Safety training, medical insurance, and health and wellness programs increase Employee health and well-being.

2. Inclusive hiring policies and competitive salaries lead to a positive impact on the local community’s work security.

3. Your company’s high standards for working conditions and collaboration with industry partners on improving working conditions positively change the industry working conditions and aid in employee well-being.

Examples of possible negative Impacts related to Working conditions (Own workforce):

1. Longer working hours and little focus on health impacts from labor activities decrease employee health and well-being.

2. Bad and unsafe working conditions negatively influence employee safety, health, and well-being.

3. Your lack of attention to working conditions negatively influences the entire industry’s reputation and culture.

4. Payment of wages does not meet the basic needs of workers and their families.

5. Failing to adapt machinery, equipment, working time, and work processes to the physical and mental capacities of the workforce.

Examples of financial opportunities related to Working conditions (Own workforce):

1. Enhanced productivity due to good working conditions and high employee well-being.

2. Low accident/injury/illness-related costs due to low rates of illness and very few accidents.

3. Lower operational costs due to high employee satisfaction caused by great working conditions and opportunities within the company.

Examples of financial risks related to Working conditions (Own workforce):

1. Lower productivity and, therefore, higher operational costs due to overworked and unhealthy employees.

2. High turnover and difficulty keeping employees due to a bad reputation - lead to higher HR costs and, eventually, a decrease in sales.

3. Higher costs related to injuries and disabilities because of the bad working conditions.

Equal treatment and opportunities for all:

Examples of possible positive Impacts related to Equal opportunities (Own workforce):

1. Higher representation of women and minorities due to strong DEI policies.

2. Positive impact on local communities through philanthropy and enhanced business ethics due to a diverse workforce.[2]

3. Enhanced climate strategies and operational eco-efficiency caused by higher diversity in management[3]

Examples of possible negative Impacts related to Equal opportunities (Own workforce):

1. Little to no opportunity for women and minorities to influence the future of your company (due to less opportunity for them to enter management positions).

2. Gender-based violence and harassment, including sexual harassment.

3. Wage discrimination for equal work or work of equal value.

4. Discrimination against workers with respect to employment or occupation on grounds such as race, color, sex, religion, political opinion, national extraction, social origin, or other status.

5. Less competitive skills or a workforce that falls behind industry trends and developments due to a lack of training and skill development opportunities.

Examples of financial opportunities related to Equal opportunities (Own workforce) :

1. Enhanced productivity and better financial performance due to high levels of gender and ethnic diversity. [4]

2. Reduction in operational costs, enhanced retention, and talent attraction due to robust DEI policies.

Examples of financial risks related to Equal opportunities (Own workforce) :

1. Loss of sales due to reputational damage or loss of competitive advantage.

2. Costs related to litigation and non-compliance with DEI regulations.

Other work-related rights:

Examples of possible positive Impacts related to Other work-related rights (Own workforce) :

1. Your company’s focus and transparency around modern slavery in your operations inspire Industry-wide efforts to end modern slavery and child labor.

2. Enhanced personal data protection through strong data-security policies and investments in safer technological solutions.

Examples of possible negative Impacts related to Other work-related rights (Own workforce):

1. Personal data leakage.

2. Incidents of forced labor or child labor.

Examples of financial opportunities related to Other work-related rights (Own workforce):

1. Enhanced productivity due to adequate housing of employees and high employee well-being.

2. New market opportunities for more sustainable and ethical products.

3. Increased sales due to a strong reputation as an ethical brand.

Examples of financial risks related to Other work-related rights (Own workforce):

1. Loss of sales due to reputational damage.

2. Costs related to litigation caused by the discovery of forced labor in operations.

3. Disruptions in business operations due to inadequate, unsafe housing of employees.

Overview of Workers in the Value Chain:

The objective of the standard Workers in the value chain is to enable users of the sustainability report to understand how the company depends on and impacts employees in their value chain, including how well the company complies with international human rights instruments and conventions, as well as the financial impact of this relationship with the workers in their value chain. Disclosure requirements in the standard will ask for your company’s policies related to your value chain workers, the approach to human rights, engagement with workers in the value chain, measures to remedy negative impacts, and how these processes and policies are monitored.

Examples of the potential Financial Impacts, Risks, and Opportunities related to Workers in the value chain can be similar to those mentioned above for your Own Workforce. However, they will be related to the workers in the value chain instead of workers in your own workforce, and depending on your company, industry, and geographical location, you might have higher potential impacts related to child labor, forced labor, and/or bad working conditions, as well as equal opportunities in your value chain than in your own operations. A good way to start to understand this is to analyze the potential impacts, risks, and opportunities(IROs) related to the raw materials that you source/ depend on in order to deliver your products and/or services. It is also important in this process to understand the geographical locations where you/your business partners source these raw materials. This standard will give you the opportunity to disclose information about how you are actively working to respond to actual/or potential impacts, risks, and opportunities related to the workers in your value chain.

So, what are some specific examples of impacts, risks, and opportunities related to Workers in the value chain that you might want to consider during the double materiality assessment (in addition to the ones mentioned for your own workforce above)?

Examples of important Negative Impacts related to Workers in the value chain:

1. Negative impact on young workers, female workers, and migrant workers in the value chain where women, young adults, and/or migrant workers are being discriminated against or exploited ( For example, certain sectors such as apparel, electronics, tourism, health and social care, domestic work, agriculture, and fresh cut flowers have more female employees and can therefore be disproportionally impacted by gender issues) [5]

2. Any incidents of forced labor, modern slavery, negative human rights impacts, or child labor.

Examples of important Financial Risks related to Workers in the value chain:

1. Low-quality products can lead to decreased sales and a damaged reputation. Selling goods premised on the cheapest price for customers creates extreme price pressure, which can lead to subcontracting, lower-quality products, and less transparent and controllable supply chains. This, again, can lead to an eventual decrease in sales and a harmful hit to the company's reputation.

2. Reputational backlash and lower sales due to low transparency and unethical supply chains.

3. Potential cost related to lawsuits caused by unethical value chains.

Overview of Affected Communities:

The objective of the Affected Communities standard is to enable users of the sustainability report to understand how the company depends on and impacts the communities connected to their own operations, value chain, products, and services. This can include communities living or working around the undertakings operating sites, factories, facilities, or other physical operations. It can also include communities affected by those sites, for example, because of downstream pollution. Affected communities can also include communities along the undertakings value chain, such as those affected by the operations of supplier facilities or by the logistic operations and distributors. Furthermore, affected communities can also be the communities at or around the point of extraction of the raw materials, like the sites around metal mines. Affected communities can also include those communities affected by the waste or recycling sites that treat the company’s products at the end of their life. Disclosure requirements in the standard will ask for your company’s policies related to affected communities, the approach to protect and ensure affected communities’ human rights, engagement with the affected communities, measures to remedy negative impacts, and /or create opportunities and positive impact and how these engagement and remediation processes & policies are being monitored. The standard also specifically asks for the company’s approach to respecting and protecting the human rights of indigenous peoples.

What are some specific examples of impacts, risks, and opportunities related to Affected Communities that you might want to consider during the double materiality assessment process?

Examples of negative impacts related to Affected communities:

1. Negative impact on indigenous peoples’ lands and indigenous peoples’ rights.

2. Any severe impact on a certain community’s livelihood and their way of sustaining themselves.

Examples of positive impacts related to Affected communities:

1. Restoration of community rights and autonomy through regenerative projects and microfinancing initiatives.

2. Your company’s focus on positively impacting affected communities inspires Industry-wide efforts to make the industry more equitable and sustainable.

Examples of financial risks related to Affected communities:

1. Risks related to legal exposure due to the loss of access to land, loss of land, or resettlements caused by supplier(s)/own operations.

2. Business interruption or disruption due to withdrawn consent or non-consent from indigenous peoples to a project on their lands, forcing the company to modify or abandon a project or operation.

3. Reputational or legal risks related to water pollution or other damage to ecosystems caused by operations or value chains.

Examples of financial opportunities related to Affected communities:

1. Access to funding from governments or communities due to the company's good reputation and its role as a partner of choice for communities, governments, or businesses.

2. The development of positive relationships between undertaking and indigenous peoples – enables existing or future projects to expand and flourish with strong support.

Overview of Consumers and End Users:

The objective of the consumer’s and end user’s standard is to enable users of the sustainability statement to understand how the company depends on and impacts the consumers/end users of their products and services. The standard's disclosure requirements will ask for your company’s policies related to consumers and end users (AND how well these align with international human rights principles), your engagement with consumers/end users, any measures to remedy negative impacts or risks, enhance opportunities and implement positive impacts, as well as, how the engagement and remediation processes are being monitored. The standard also specifically asks for the company’s approach to responsible marketing practices, whether some products or services are inherently harmful to people and can increase the risk of chronic disease, how well the company ensures the protection of customers personal data, and the company’s approach to the protection of children& other vulnerable individuals through product labels, manuals, and responsible marketing strategies.

What are some specific examples of impacts, risks, and opportunities related to Consumers and end users that you might want to consider during the double materiality assessment?

Examples of negative impacts related to Consumers and end users:

1. Goods and services do not meet all agreed or legally required standards for consumer health and safety, including requirements for health warnings and safety information.

2. Misinformation, omission of information, or any other deceptive, fraudulent, or unfair practices cause consumers to be misled.

Examples of positive impacts related to Consumers and end users:

1. Good practices for responsible marketing cause consumer trust and consumer satisfaction.

2. Products are accessible, inclusive, and safe. Product instructions allow for appropriate and safe use.

3. Your company’s focus on health, safety, and accessibility inspires Industry-wide efforts to enhance the accessibility and safety of products and services.

Examples of financial risks related to Consumers and end users:

1. Costly lawsuits caused by your company’s unsafe products and services.

3. Loss of market share and sales due to inappropriate marketing, misleading information, and/or unsafe products.

Examples of financial opportunities related to consumers and end users:

1. Access to more funding due to a strong brand reputation built by transparency and high standards for health, safety, and accessibility.

2. Increased sales due to the high accessibility and safety of your company’s products.

In the ESRS, there is only one standard under the Governance umbrella, called Business Conduct. Below is a summary to help you when conducting your double materiality assessment for Business Conduct:

Overview of Business Conduct :

The objective of the Business Conduct Standard is to enable users of the sustainability statement to understand how your company approaches and performs with respect to business conduct. The standard also specifically asks for the company’s approach to impacts, risks, and opportunities related to corporate culture, protection of whistleblowers, animal welfare, political engagement, corruption and bribery prevention, and the management of relationships with suppliers, including payment practices.

What are some specific examples of impacts, risks, and opportunities related to Business conduct that you might want to consider during the double materiality assessment?

Examples of negative impacts related to Business conduct :

1. Bribery of public officials to win public procurement contracts, obtain customs clearance, or avoid regulations and controls.

2. Poor company/corporate culture causes employee dissatisfaction and a toxic work environment.

3. Reliance on specific suppliers causes a less resilient value chain and a less competitive industry.

Examples of positive impacts related to Business conduct :

1. Strong anti-corruption policies inspire industry-wide reduction in bribery and corruption.

2. A positive company/ corporate culture causes employee satisfaction and positive work environments.

3. A focus on sourcing from diverse suppliers enhances the resilience of your supply chain and positively impacts competition and diversity in your industry.

Examples of financial risks related to Business conduct :

1. Costs related to lawsuits or legal action caused by bribery and corruption or a toxic corporate culture.

2. Business interruptions caused by heavy reliance on certain suppliers lead to a subsequent decrease in sales and profit.

Examples of financial opportunities related to Business conduct:

1. Your strong corporate culture leads to innovation and competitive advantage.

2. A resilient value chain with strong supplier relationships lowers costs.

If you read all the way to the end, I hope this post provided useful guidance for your double materiality assessment process (and more specifically -that it helped give useful guidance on how to think about the Social and Governance Topics).

My next post will review the disclosure requirements for each standard.

Sources:

[1] OECD Due Diligence Guidance for Responsible Business Conduct. OECD, 2018. Available here: https://mneguidelines.oecd.org/OECD-Due-Diligence-Guidance-for-Responsible-Business-Conduct.pdf

[2] Diversity Matters Even More: The Case for Holistic Impact. McKinsey & Company, 2023. Available here: https://www.mckinsey.com/featured-insights/diversity-and-inclusion/diversity-matters-even-more-the-case-for-holistic-impact: McKinsey found that a 10% increase in diverse representation on leadership teams is positively correlated to additional score points like a) positive community impact through a correlated increase in philanthropy, and business ethics, b) positive workforce scores through enhanced talent attraction and retention, and c) better environmental scores through correlated enhances in climate strategy and operational eco-efficiency.

[3] ibid

[4] ibid

[5] OECD Due Diligence Guidance for Responsible Business Conduct. OECD, 2018. Available here: https://mneguidelines.oecd.org/OECD-Due-Diligence-Guidance-for-Responsible-Business-Conduct.pdf